voestalpine with considerable profit increase in 3rd quarter 2009/10 compared to previous quarters

In the third quarter of 2009/10, the voestalpine Group is emerging from the crisis with a substantial increase in profit.

In the third quarter of 2009/10, the voestalpine Group is emerging from the crisis with a substantial increase in profit.

After five consecutive quarters with declining numbers, the third quarter 2009/10 shows a slight upward trend in revenue (from EUR 2,067.6 million to EUR 2,083.9 million). EBIT surges by 87.5% from EUR 70.4 million to EUR 132 million. Profit for the period with EUR 71.5 million increased by 150% compared to 2nd quarter (EUR 28.3 million).

In the course of the 2009/10 business year, we have been able to accomplish a broadly based turnaround, from a loss in the first quarter to positive figures in the second quarter to a substantial profit in the third quarter.

Even taking a cautious stance, there are many indications that the global economic crisis bottomed out in the second quarter of 2009. By the end of 2009, increasing signs of a gradual economic recovery had taken a more firm hold, and since the summer of 2009, the 2010 forecasts of the growth rates of the major economies have been progressively revised upward.

However, whether these economic uptrends actually indicate a sustainable recovery and how strong it will be is still up in the air. Both the regional and the industry-specific performance of market segments that determine economic well-being continues to be highly differentiated.

The global upswing—just like the boom prior to the economic crisis—is originating primarily in Asia, mainly China and India, as well as in Brazil, the most important South American economy. In contrast, despite the government-backed stimulus programs, unprecedented in the level of their funding, the recovery in the USA and Europe has been substantially delayed and its momentum has been comparatively weak. It should be noted, however, that the quickly implemented government-run incentive programs, such as the ones to stimulate automobile production or the construction industry, did have a direct effect in many countries. In a regional comparison, the market environment in Eastern Europe, including Russia, continues to be very subdued.

Not unlike the individual economic regions, the performance of the major customer industries is also quite dissimilar. Generally speaking, some of the demand during the past months in many industries has been due to the (partial) replenishment of very low inventories. Nevertheless, all in all the inventory situation—apparently driven by rigorous liquidity management policies—continues to be characterized by low inventory levels rather than surpluses.

In the footsteps of overall economic developments, global steel production began to recover in the summer of 2009, with China’s unabated demand again the driving force. With demand somewhat reenergized, worldwide production capacity that had been temporarily shut down was quickly reactivated, resulting in tougher price competition in several regions—primarily in Europe—toward the end of 2009. The current state of the markets for coal, ore, and coke is driven by strong growth in the emerging markets, which has led to a considerable increase of the spot market prices; as a result, a massive increase of the contract prices, which will be renegotiated beginning in April 2010, can be expected.

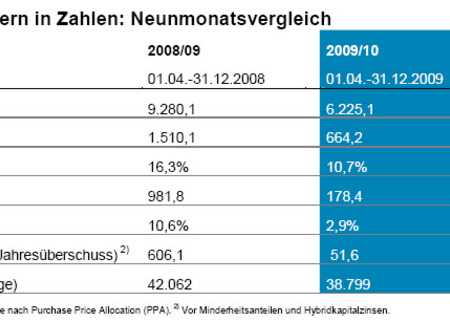

During the first three quarters of 2009/10, the Group’s revenue fell by EUR 3,055 million (-32.9%) from EUR 9,280.1 million to EUR 6,225.1 million. In evaluating the current economic development, a comparison of the third quarter of 2009/10 with the immediately preceding quarter (second quarter of 2009/10) has far more informative value than a nine-month comparison. While all reporting categories showed a trend reversal as early as the second quarter of 2009/10, the turnaround as far as revenue is concerned did not occur until the third quarter of 2009/10, and even then, at EUR 2,083.9 million, earnings were barely 1% higher than in the quarter immediately preceding it (EUR 2,067.6 million).

In comparison to an operating result (EBIT) of EUR 981.8 million in the first three quarters of 2008/09, for the same period of 2009/10, the voestalpine Group recorded a result that fell to EUR 178.4 million, a reduction by 81.8%. Considering the economic circumstances, however, this a satisfactory result that corresponds to an EBIT margin of 2.9% (after 10.6% in the previous year).

When reviewing the quarters individually, it becomes clear that a trend reversal began in second quarter of 2009/10 (first quarter of 2009/10: EUR -24 million) with an EBIT of EUR 70.4 million and continued in the third quarter of 2009/10, with EBIT going up by 87.5% to EUR 132.0 million; the EBIT margin rose from the second to the third quarter from 3.4% to 6.3%. As was the case in the second quarter, only the Special Steel Division recorded negative figures in the third quarter of 2009/10 with EUR -22.5 million EUR (penalized by the purely accounting effects of the ppa).

Although the profit before tax and the profit after tax (profit for the period)1 were already positive in the second quarter of 2009/10, nevertheless, the first half of 2009/10 showed negative figures at EUR -38.4 million and EUR -19.9 million, respectively. Due to the significant improvement of the operating result in the third quarter of 2009/10, the figures both for the before tax result and the profit for the period were positive in the first three quarters of 2009/10, with the Group recording EUR 51.2 million (after EUR 764.7 million in the previous year) as profit before tax and EUR 51.6 million (after EUR 606.1 million in the previous year) as profit after tax (profit for the period).

For the first three months of 2009/10, earnings per share (EPS) were EUR -0.05 per share (previous year: EUR 3.36)2, respectively, EUR 0.30 per share for the third quarter of 2009/10.

Equity went down in the first three quarters of 2009/10 compared to March 31, 2009 by 4% from EUR 4,262.5 million to EUR 4,091.6 million. This decline is due largely to dividend payments to shareholders and owners of hybrid capital in the amount of EUR 246.8 million. Due to investment expenditure that was lower than depreciation and very significantly decreased working capital (-28.5%) compared to March 31, 2009, net financial debt (in % of equity) was reduced from EUR 3,761.6 million to EUR 3,323.5 million. Thus, as of December 31, 2009, the voestalpine Group’s gearing ratio (net financial debt as a percentage of equity) was 81.2%. The substantial reduction of the gearing ratio compared to both March 31, 2009 (88.2%) and September 30 (90.0%) reflects the Group’s strong self-financing capability and its consistent liquidity management despite the challenging economic circumstances and a dividend policy that has been consistently applied.

The Group’s crude steel production in the first three quarters of 2009/10 was 4.44 million tons, 22.5% below the previous year’s corresponding figure (5.73 million tons).

In the first three quarters of the 2009/10 business year, the investments of the voestalpine Group amounted to EUR 381.3 million. Investments are now lower than depreciation and almost 50 % lowar than in the previous year. However, it should be emphasized that those investment projects focused on the expansion of the Group’s leadership role in both technology and quality are still being vigorously pursued.

There were no acquisitions or divestments during the 3rd quarter of the 2009/10 business year.

As of December 31, 2009, the voestalpine Group had 38,799 core employees worldwide (not including apprentices). Compared to December 31, 2008 (42,062), this corresponds to a decrease by 7.8% or 3,263 employees. In addition to the reduction of core staff, the number of leased personnel was reduced by 445 employees. Furthermore, as of December 31, 2009, 4,140 employees were still on reduced working hours; compared to September 30, 2009 (4,851 employees), 711 employees have been able to resume their regular working hours due to improved capacity utilization.

In consideration of all measures that were taken, both with regard to core and leasing employees, the number of staff has been reduced due to the economic crisis as compared to December 31, 2008 by 11.3%; compared to the number of employees at the very beginning of the crisis in September 2008, the total reduction comes to 15.5%.

In the interest of securing the future of the company in the long term, the voestalpine Group continues to adhere to its apprenticeship program, both with regard to quantity and quality, despite the crisis. As of December 31, 2009, 1,718 apprentices were being trained, only 49 less than in the previous year.

With the publication of the EU’s Climate and Energy package on June 5, 2009, the future direction for an ambitious reduction in CO2 emissions throughout the European Union to 2020 and beyond has been set. As an industry that is part of the “carbon leakage” segment, the steel sector is set to be allocated free emission certificates according to strict benchmarks for up to a total of 100% based on sectoral allocation options; adjustments based on the results of the next World Climate Conferences are possible. No concrete measures can be derived from the World Climate Conference held in Copenhagen in December 2009. From the perspective of European industry, the participants neglected in particular to persuade the major non-European CO2-emitting nations to accept the same or at least similar CO2 reduction levels to which the European Union has already committed itself. This will mean a significant deterioration of the competitive situation for European industry with regard to CO2 costs unless it is possible to reach agreement on an appropriate global adjustment at the next climate conferences. The setting of a future course that was anticipated for Copenhagen has been postponed to the next conference at the end of 2010 in Cancún, Mexico; this means that with regard to future investments, there is a state of uncertainty concerning the regulatory framework, making reliable planning impossible.

The benchmark system recommended by voestalpine AG jointly with the European steel association EUROFER and its member companies is currently being negotiated with the European Commission. The basis for this benchmark system is a comprehensive collection of data regarding all plants and facilities of the European steel industry that will be affected by CO2 certificate trading from 2013 on.

The post-crisis economic recovery that began in China during the summer of 2009 has also been underway in Europe since the fall of 2009, albeit, for the time being, with much diminished momentum. With over two thirds of revenue being generated in Europe, this remains the voestalpine Group’s most important market region. As explained at the beginning of this letter to shareholders, the speed and extent of the upward trend vary greatly, as the picture is extremely differentiated, both according to countries and economic sectors. While recovery has been slow in Western, Southern, Central, and Eastern Europe, positive economic signs have been increasingly encouraging in the German-speaking countries, the Benelux countries, and Northern Europe.

The situation in the most important customer industries is similarly uneven. In the automobile industry, the revival of demand continued, primarily in the premium segment, although prices have been highly competitive. In the energy segment, solar and wind energy have been booming (not least due to massive government subsidies) and the first positive signs of increased demand are becoming noticeable in the conventional energy segment as well, although the generator segment continues to stagnate. In the machine manufacturing and commercial vehicle industries, the upward trend has been limited only to a low-level consolidation. All in all, performance in the European construction and construction supply industries continues to be merely average, although trends differ significantly depending on region and sector. For example, demand in the railway infrastructure segment is stable at quite a good level in the EU-15 member states, while in Central and Eastern Europe, it has fallen sharply in the past several quarters. The market in the home appliance segment shows a similar east-west gradient. The aviation industry overall will stay under the influence of a weak market environment for quite some time, not just in Europe, but worldwide.

Compared to the outlook in the last quarterly report, the economic situation in Europe has improved in individual segments and regions, however, it is still too early to speak of a broad or sustainable recovery. Nevertheless, throughout 2010, the recovery should gradually gain momentum and the danger of a broad-based economic setback lessen. This development is being driven by increasing economic consolidation in Western Europe on one hand, and on the other, by the regained economic momentum in Asia and South America, as well as an economic uptick in the USA. The majority of the Central and Eastern European countries, however, will be able to follow this trend only with some delay, due to the structural deficits in their economies. The falling rate of exchange of the euro vis-à-vis the US dollar and some other currencies helps exports and is beneficial for an economic recovery in Europe.

Against this backdrop, continuously improving capacity utilization is anticipated for all five divisions of the voestalpine Group, to the extent that they are not already working at full capacity (such as the Steel Division). Driven by the expected massive price increases for coal and ore, significant increases in earnings along the Group’s entire value chain are being anticipated for 2010. The voestalpine Group should be able to conclude the 2009/10 business year with a clearly positive operating result (EBIT), as well as a positive profit for the period (net income).

1 Before minority interests and interest on hybrid capital.

2 Basis of the calculation is the profit for the period; in the letter to shareholders for the third quarter of the 2008/09 business year, the basis for calculation was the profit for the period from continuing operations at EUR 3.40 per share.